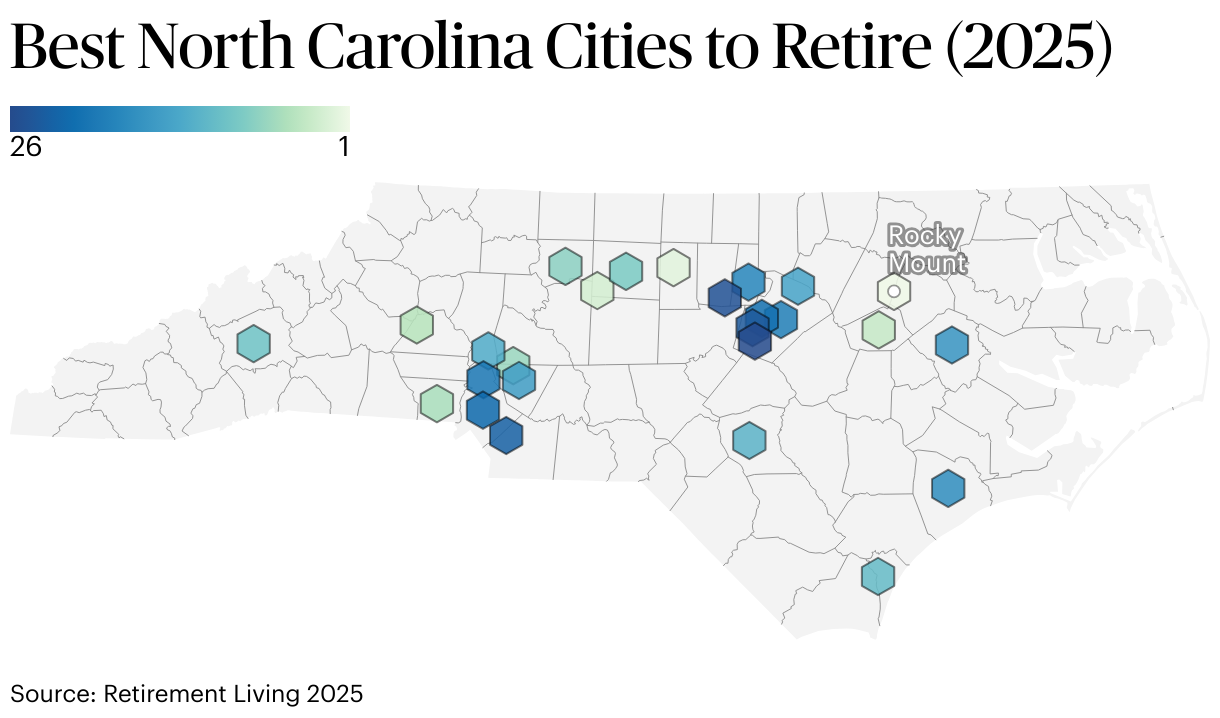

Best Cities to Retire in North Carolina

Best Cities to Retire in North Carolina

Updated:

May 30, 2025

Open Access

From the energy of its vibrant cities to the tranquility of mountain towns and the laid-back charm of its coastal communities, North Carolina really feels like home in every corner.

Combine that with a low average property tax rate of 0.73% and no tax on Social Security benefits, and it’s easy to see why so many older adults are eyeing North Carolina as a place to settle in.

Key Insights

Rocky Mount ranks as the best city to retire in North Carolina, with the highest share of residents aged 65+ and the lowest housing costs on the list.

↓ Jump to insight

Kannapolis stands out for its financial stability, with the lowest poverty rate among the top 10 cities, although it also has higher housing costs.

↓ Jump to insight

Asheville is the most expensive city to retire in among our top 10, with the highest median home and rent prices.

↓ Jump to insight

With so many different cities to choose from, we want to help you narrow down your options. We’ve ranked the top 10 best cities to retire in North Carolina based on factors like housing costs, senior population, poverty rates, and local sales tax.

Top 10 Cities to Retire in North Carolina

Here’s how the top 10 cities in North Carolina line up for retirees:

1. Rocky Mount, North Carolina

- Share of population 65+: 20.2%

- Median home sale price: $180,000

- Median rent price: $919

- Poverty rate: 21.2%

- Sales tax: 6.75%

Rocky Mount sits between Edgecombe and Nash counties. Roughly 20.2% of the population here is aged 65 or older, which is the highest share on this list. Rocky Mount also stands out for being the most affordable city to retire with a median home price of around $180,000, and median rent is just $919. Few places in North Carolina offer this kind of breathing room.

For retirees who want to stretch their savings, stay active, and be part of a senior-friendly community, Rocky Mount offers real value.

2. Burlington, North Carolina

- Share of population 65+: 18%

- Median home sale price: $264,000

- Median rent price: $1,030

- Poverty rate: 18%

- Sales tax: 6.75%

Right in the heart of North Carolina, Burlington is perfectly positioned for those who want to stay connected and explore the state with ease

Around 18% of Burlington’s population is 65 or older, which means you’re likely to find neighbors in the same stage of life and plenty of ways to stay active and social.

The sales tax is 6.75%, which helps with day-to-day costs. That said, the poverty rate is 18%, so the level of financial stability can vary depending on the area.

3. High Point, North Carolina

- Share of population 65+: 16.1%

- Median home sale price: $255,000

- Median rent price: $1,062

- Poverty rate: 14.7%

- Sales tax: 6.75%

High Point, set in Guilford County, is famously known as “The Furniture Capital of the World” thanks to its deep roots in furniture manufacturing. But what stands out more for retirees is its balance between affordability and stability.

The median home price is $255,000, making it easier to buy without dipping too far into retirement savings. Plus, it also has a poverty rate of 14.7%, making it one of the more financially secure places on this list. That can mean better-funded local services that you can rely on.

About 16.1% of the population is 65 or older, which is lower than in some other cities on our list. While the city feels lively and community-oriented, certain neighborhoods may cater more to families than to retirees.

4. Wilson, North Carolina

- Share of population 65+: 17.9%

- Median home sale price: $249,500

- Median rent price: $925

- Poverty rate: 25.1%

- Sales tax: 6.75%

Wilson has that small-town feel while being just a short drive from Raleigh, giving residents the best of both worlds.

With 17.9% of the population aged 65 and older, Wilson ranks fourth in terms of retiree presence. Affordability is another plus; the median home price is about $249,500, and the median rent is $925, making it a wise choice for retirees looking to stretch their budgets. But it’s not without trade-offs. The poverty rate is 25.1%, which is the highest on this list. That could mean more visible economic challenges or fewer resources in some areas.

5. Hickory, North Carolina

- Share of population 65+: 16.6%

- Median home sale price: $312,000

- Median rent price: $975

- Poverty rate: 16.9%

- Sales tax: 7%

Set against the foothills of North Carolina, Hickory combines scenic beauty with a warm, down-to-earth charm that will make you feel at home.

The city has a large senior population with 16.6% of residents aged 65 or older.

Housing costs are higher here; the median home price is $312,000; however, median rent is more manageable at $975. For those who are not ready to buy, renting may provide more flexibility.

Hickory also has a 7% sales tax, which is among the highest on this list and can chip away at your monthly budget.

6. Gastonia, North Carolina

- Share of population 65+: 15.1%

- Median home sale price: $296,000

- Median rent price: $1,145

- Poverty rate: 14.3%

- Sales tax: 7%

Just west of Charlotte, Gastonia combines suburban comfort with access to big-city perks. It’s the largest city in Gaston County and has built a reputation for being both livable and lively.

With a poverty rate of just 14.3%, it ranks as the second-most financially stable spot among our top 10. That can translate into better public services and a safer, more reliable environment.

That said, it’s not the cheapest place to live. Median home prices are around $296,000, and median rent comes in at $1,145. Add a 7% sales tax, and your day-to-day expenses can stack up fast.

7. Kannapolis, North Carolina

- Share of population 65+: 14.9%

- Median home sale price: $324,945

- Median rent price: $1,168

- Poverty rate: 12.2%

- Sales tax: 7%

Kannapolis has a polished feel, with quiet neighborhoods and plenty of green space. You’re within driving distance of mountains and bigger cities without being in the middle of the noise.

It is also the most financially stable city in our top 10, with a poverty rate of 12.2%. However, it’s not the most affordable place to settle. Median home prices are around $324,945, and median rent is $1,168, both are the second highest among our top 10.

8. Winston-Salem, North Carolina

- Share of population 65+: 14.8%

- Median home sale price: $280,500

- Median rent price: $1,033

- Poverty rate: 17.9%

- Sales tax: 7%

If housing costs are a priority, Winston-Salem delivers. The median home price is around $280,500, and the median rent is about $1,033. Both are strong options for retirees seeking value without compromising on quality of life.

While only 14.8% of residents are 65 or older, which might mean fewer senior-specific amenities or social groups, the city still offers a welcoming atmosphere and access to essential services.

Keep in mind that the 7% sales tax can add up, especially if you’re on a fixed income. Still, for retirees wanting an affordable place to settle, without the hustle of a big city, Winston-Salem is worth considering.

9. Greensboro, North Carolina

- Share of population 65+: 13.9%

- Median home sale price: $283,500

- Median rent price: $1,114

- Poverty rate: 18.4%

- Sales tax: 6.75%

Greensboro offers a well-rounded slice of North Carolina, with easy access to both the mountains and the beach.

Everyday expenses are a bit easier here too, it’s 6.75% sales tax, ties for the lowest among our top 10, providing a small but steady advantage for long-term budgeting.

However, with seniors making up just 13.9% of the population, the smallest share among our top 10, Greensboro may feel a bit youthful for those seeking a stronger retiree community.

Plus, the city has a poverty rate of 18.4%, so it’s worth exploring neighborhoods carefully to find the stability and support you need.

10. Asheville, North Carolina

- Share of population 65+: 19.2%

- Median home sale price: $547,500

- Median rent price: $1,303

- Poverty rate: 14.6%

- Sales tax: 7%

Asheville sits between the Appalachian and Blue Ridge Mountains, blending scenic beauty with deep-rooted history.

About 19.2% of the population is 65 or older, so you’ll find a well-established senior community here. It’s easier to meet people and settle into a retirement routine that doesn’t feel isolating. With a poverty rate of 14.6%, it’s also more financially stable than many other cities across the state.

However, this natural charm comes at a price. Median home sale prices are the highest among our top 10 at $547,500, and median rent is $1,303. If Asheville is on your shortlist, it’s worth taking a closer look at your long-term budget. The lifestyle here is rich, but it does ask for planning.

See Where Your North Carolina Community Ranks for Retirement

Curious where your city stands? Below is the full list of the largest cities in North Carolina, ranked based on factors that matter most for retirees.

Methodology

We looked at North Carolina cities with at least 40,000 people and compared them using key retirement-friendly factors. These included home prices, rent, local tax rates, poverty levels, and the share of residents aged 65 and older. Each factor was weighted based on how much it tends to shape day-to-day life in retirement.

The numbers came from reliable and recent sources. Population, rental costs, and poverty rates are from the 2023 American Community Survey (5-Year Estimates). Home sale prices reflect Redfin’s April 2025 data, while sales tax information was pulled from Avalara.

Here’s a breakdown of how each factor influenced our rankings:

- Percentage of Population 65+: 30%

- Median Home Sale Price: 20%

- Median Monthly Rent: 20%

- Poverty Rate: 20%

- Sales Tax: 10%

Reference Policy

If you find this information useful, you can share it for non-commercial purposes. However, we request that you include a link back to this page to give proper credit.

Article Sources

- 2023 American Community Survey 5-Year Estimates

- Redfin

- Avalara

Read More

Are you considering retiring somewhere other than North Carolina? You can explore our guide to the 10 Best U.S. Cities for Retirement and our Best and Worst States to Retire In.

Will your savings last through retirement? Here’s how to improve your odds

Will your savings last through retirement? Here’s how to improve your odds

45% of Americans fear their retirement savings won’t last a lifetime

Updated:

Key Insights

- Establish a flexible, sustainable spending rate that aligns with your goals and life expectancy.

- Let your investments grow by balancing safety with long-term performance potential.

- Plan ahead for healthcare and long-term care costs, which can take up a significant portion of your retirement budget.

For nearly half of American retirees, one question casts a long shadow: “Will I outlive my money?” According to Merrill Lynch research, 45% of Americans fear their retirement savings won’t last a lifetime. But with proactive planning and smart adjustments, retirees can gain control over their financial future.

“Retirement planning isn’t about predicting the future perfectly—it’s about being prepared to adapt,” says Eric Breemen, a financial advisor with Merrill.

Here are three key steps that can help make your savings stretch further and smarter.

Step 1: Develop a sustainable spending strategy

The conventional wisdom of withdrawing 4% annually from your retirement savings is a helpful guideline, but not a one-size-fits-all rule. Many retirees may need to adjust that rate depending on:

- Their retirement age

- Health status and life expectancy

- Other income sources like Social Security or pensions

Annual withdrawals

For instance, someone with $1 million in savings using a 4% withdrawal rate would have $40,000 to spend in their first year of retirement. However, if you expect to live well into your 90s or have a family history of longevity, a more conservative rate of 3% to 3.5% may be wise. Women, who statistically live longer than men, might especially benefit from a lower drawdown rate.

If your budget looks tight, consider delaying Social Security benefits until age 70 or working longer to increase your future income.

Step 2: Let your investments do the work

Many retirees play it safe by leaning heavily into low-risk assets like bonds and CDs. But being too conservative can backfire. Over a 30-year retirement, cash-heavy portfolios may not keep up with inflation, especially with rising healthcare costs.

Build a smarter strategy:

- Maintain a diversified portfolio that includes stocks and bonds for growth.

- Create a “liquidity bucket”—a reserve of 2–3 years’ worth of expenses in safe, liquid accounts—to provide peace of mind during market downturns.

- Hedge against inflation with assets like Treasury Inflation-Protected Securities (TIPS), real estate, or commodities like gold.

For example, without inflation protection, $1 million in cash could lose nearly 40% of its value over 25 years. Strategic investment choices are essential to preserving—and growing—your nest egg.

Step 3: Prepare for healthcare and long-term care costs

Healthcare is one of the biggest wild cards in retirement spending. About 70% of Americans over 65 will need some form of long-term care, and a semi-private nursing home room now averages over $111,000 per year.

If you don’t have long-term care insurance, it’s essential to set aside a portion of your savings specifically for future medical expenses. Options include:

- Health Savings Accounts (HSAs) for tax-free medical spending

- Dedicated investment accounts for healthcare planning

- Hybrid insurance policies that combine life and long-term care benefits

Understand what Medicare covers—and what it doesn’t—so you can fill any gaps without depleting your core retirement funds.

Most importantly, don’t let emotions derail your financial strategy. Markets may fluctuate, and personal priorities can shift, but having a flexible, well-structured plan will help you stay on track.

“Regular check-ins with your advisor can help you adjust for changes in life or the market,” says Anil Suri, managing director at Merrill. “These timeless principles of spending wisely, investing strategically, and planning for the unexpected are the backbone of lasting financial health.”

The amount needed to retire comfortably isn’t the same everywhere. Use our state-by-state breakdown to see the retirement savings needed in your state. By staying informed and making deliberate choices, you can enjoy your retirement years with greater confidence and peace of mind.

Approaching retirement? Here’s how to plan for your Social Security benefits

Approaching retirement? Here’s how to plan for your Social Security benefits

One of the most important decisions is when to start drawing benefits

Updated:

As retirement approaches, making informed decisions about your Social Security benefits can significantly impact your financial stability and healthcare coverage for years to come. The Social Security Administration (SSA) has offered tools and guidelines to help future retirees make the most of their benefits. Whether you’re considering when to apply, how healthcare will factor in, or what taxes to expect, thoughtful planning is essential.

Here are three key areas to focus on as you prepare for retirement:

- You can begin collecting Social Security retirement benefits anytime between ages 62 and 70. However, the amount you receive monthly depends on when you start.

- Early application (as soon as age 62) results in smaller monthly payments.

- Delaying until age 70 means your benefit amount will be at its highest.

- Your decision should reflect your personal needs, health, income, and family situation.

Knowing your Full Retirement Age (FRA), which ranges from 66 to 67 depending on your birth year, is crucial. For example, if you apply before your FRA and are still working, your benefits could be temporarily reduced if your earnings exceed a certain limit.

Understand the financial impacts

Use your Social Security online account to see how your benefit amount changes depending on when you apply. This helps you decide on the best time based on your income needs and life expectancy.

If your combined income exceeds $25,000 (single) or $32,000 (married filing jointly), you may owe federal income taxes on your benefits. You can opt to have taxes withheld from your payments to avoid a surprise tax bill.

Working before your Full Retirement Age may reduce your Social Security payments if your income surpasses annual limits. After reaching your FRA, however, you can earn as much as you want without affecting your benefits.

Plan for healthcare coverage

At age 65, you become eligible for Medicare. Signing up for Part B (medical insurance) will result in a monthly premium deduction from your Social Security check. To avoid any disruption in coverage or surprises in your benefit amount, it’s wise to plan for this expense well in advance.

Also, your benefit may be affected by whether you’re eligible for spouse or survivor benefits—these have unique rules and timelines. For example, spouse benefits max out at your Full Retirement Age and don’t increase if delayed beyond that.

Final tip

To avoid a gap in income, apply for your benefits up to four months in advance of when you want your first payment. For instance, if you want your first check in April, you can apply as early as November of the previous year.

By reviewing your benefit estimates, planning for healthcare costs, and understanding tax and earnings implications, you can set yourself up for a more secure and predictable retirement. Start planning today to make the most of the benefits you’ve earned.

Social Security recipients face a threat from delinquent student loans

Social Security recipients face a threat from delinquent student loans

They could see a 15% reduction in their monthly benefits

Updated:

Key Insights

- Social Security recipients with delinquent student loans may face a 15% reduction in monthly benefits, even if it’s their only source of income, due to federal garnishment policies.

- More than 100,000 retirees were impacted by benefit offsets in 2024, with many left below the poverty line, highlighting the severity of the issue.

- Advocates urge reforms such as easier hardship exemptions and debt relief for vulnerable seniors, while recipients are encouraged to act early to avoid default.

Student loan payments, deferred during the pandemic, have resumed, and it could be a painful shock for some Social Security recipients. Retired Americans relying on Social Security for their primary source of income may face unexpected financial hardship if they have delinquent student loan debt, either for their education or for their children’s.

The federal government continues to enforce policies that allow student loan defaults to trigger Social Security benefit garnishments, threatening the financial stability of older borrowers.

According to the Government Accountability Office (GAO), tens of thousands of Social Security recipients are subject to benefit reductions each year because of unpaid federal student loans. The Department of the Treasury is authorized to withhold up to 15% of a monthly Social Security payment through a process known as the Treasury Offset Program. This reduction can occur even if the recipient depends solely on these benefits to survive.

Older Americans face a combination of skyrocketing education costs, long-term repayment plans, and compounding interest that leaves some with loan balances they can’t feasibly pay off. Some borrowers took out loans to help children or grandchildren attend college, while others went back to school later in life. Either way, if payments are missed and loans fall into default, the government can—and does—intervene.

A 2024 Congressional Budget Office (CBO) report estimated that nearly 114,000 retirees had their benefits garnished during the previous year alone. Many received as little as $750 per month after the offset—well below the poverty line. While hardship exemptions exist, they can be difficult to obtain and are not automatically granted.

Advocates call for reform

Consumer rights groups and some lawmakers are calling for reforms to protect vulnerable retirees from punitive debt collection. Proposals include raising the protected income threshold, simplifying the hardship exemption process, and canceling debts for the most financially fragile borrowers.

Older Americans worried about student debt should take proactive steps to avoid garnishment:

- Contact your loan servicer early to explore options like income-driven repayment or consolidation.

- Apply for hardship exemptions if Social Security is your only source of income and you’re at risk of garnishment.

- Monitor your loan status to avoid default, as garnishments only occur once a loan is in default.

Here’s how the House-passed tax bill would affect retirees

Here’s how the House-passed tax bill would affect retirees

Social Security benefits are still taxed, but there’s a new tax deduction

Updated:

Key Insights

- The bill increases the standard deduction by $4,000 for retirees 65 and older through 2028, eliminates federal income taxes on tips and overtime (benefiting part-time working retirees), and makes the 2017 tax cuts permanent, providing long-term tax planning stability.

- Proposed $1.2 trillion in cuts to Medicare and Medicaid could result in reduced services and higher costs for seniors, while new Medicaid work requirements starting in 2026 may impact low-income retirees.

- The bill blocks a rule requiring 24/7 registered nurses in nursing homes, potentially affecting care quality, but preserves the favorable annuity calculation method for federal retirees under the FERS system.

The “One Big Beautiful Bill Act” (H.R. 1), recently passed by the House of Representatives, introduces a series of tax reforms and spending adjustments that carry significant implications for retirees across the United States.

Things that benefit retirees:

- Enhanced Standard Deduction: Retirees aged 65 and older will see an increase in the standard deduction by $4,000 through 2028. This adjustment aims to reduce taxable income for seniors, potentially lowering their overall tax burden.

- Elimination of Taxes on Tips and Overtime: The bill removes federal income taxes on tips and overtime pay. While primarily benefiting active workers, this provision may also aid semi-retired individuals who continue to work part-time in service industries.

- Extension of 2017 Tax Cuts: The legislation makes permanent several individual tax provisions from the 2017 Tax Cuts and Jobs Act, including reduced income tax rates across most brackets. This permanence provides long-term tax planning stability for retirees.

Healthcare and social program adjustments

To offset the projected $3.8 trillion increase in the national deficit over the next decade, the bill includes significant reductions in federal spending. Notably, it proposes nearly $700 billion in Medicaid cuts and could trigger approximately $500 billion in automatic Medicare cuts between 2027 and 2034 due to statutory Pay-As-You-Go (PAYGO) rules. These cuts may lead to reduced services and higher out-of-pocket costs for seniors.

Starting in December 2026, able-bodied adults without dependents will be required to fulfill 80 hours per month in employment or community activities to maintain Medicaid eligibility. This change could affect low-income seniors who rely on Medicaid for healthcare coverage.

The bill seeks to block a Biden-era rule mandating 24/7 registered nurse presence in nursing homes, potentially affecting the quality of care for residents, many of whom are elderly.

Federal retirement benefits

FERS Annuity Calculation: A proposed change to calculate the Federal Employees Retirement System (FERS) annuity based on the highest five years of salary instead of the highest three was removed from the final bill. This decision preserves the current calculation method, which is more favorable to federal retirees.

While the “One Big Beautiful Bill Act” offers certain tax benefits to retirees, the potential reductions in Medicare and Medicaid funding raise concerns about the accessibility and affordability of healthcare for seniors. As the bill moves to the Senate, further deliberations and amendments are anticipated, which could alter its impact on the retiree population.

Retirees are encouraged to consult with financial advisors to understand how these changes may affect their circumstances and to plan accordingly for potential shifts in healthcare costs and tax liabilities.

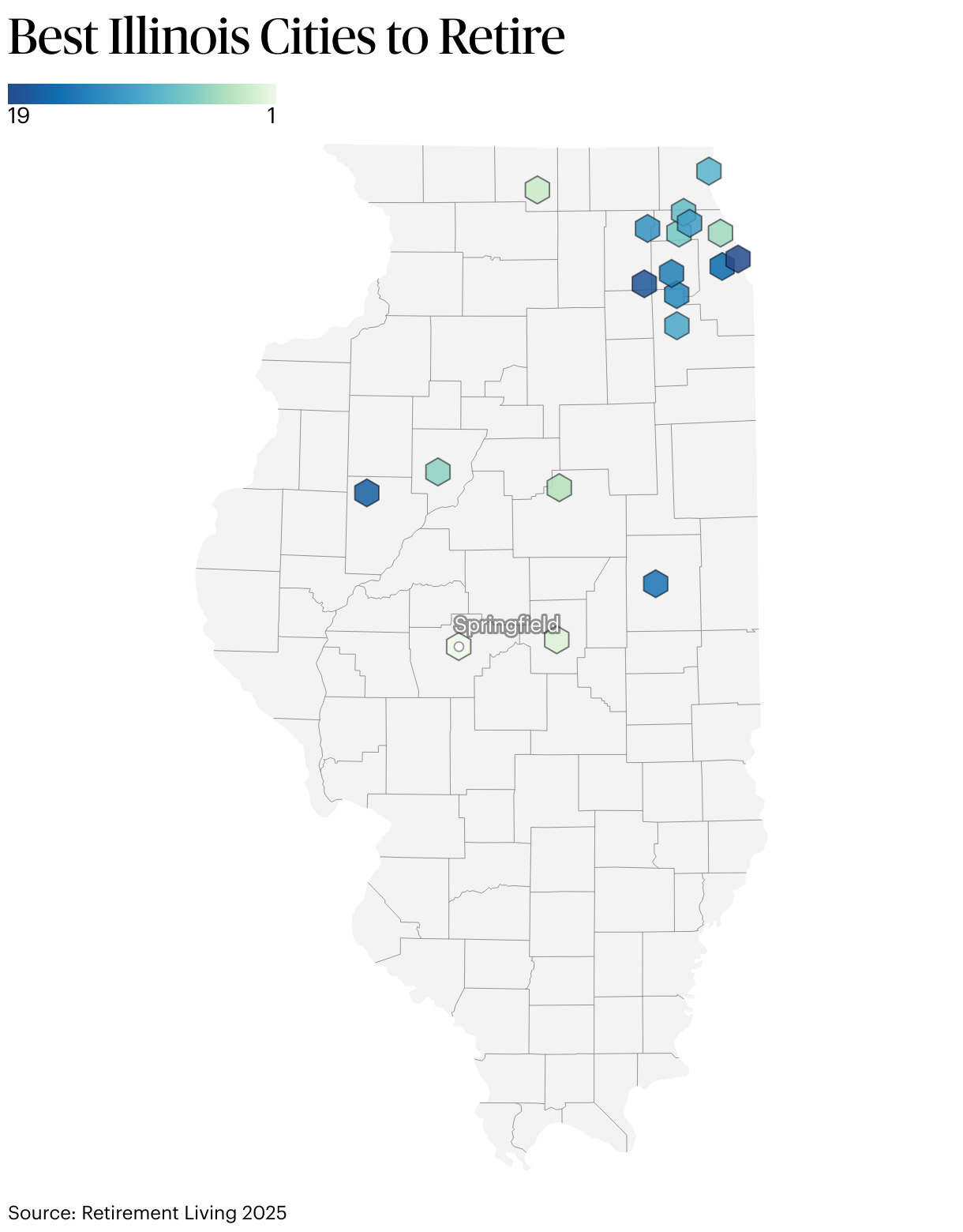

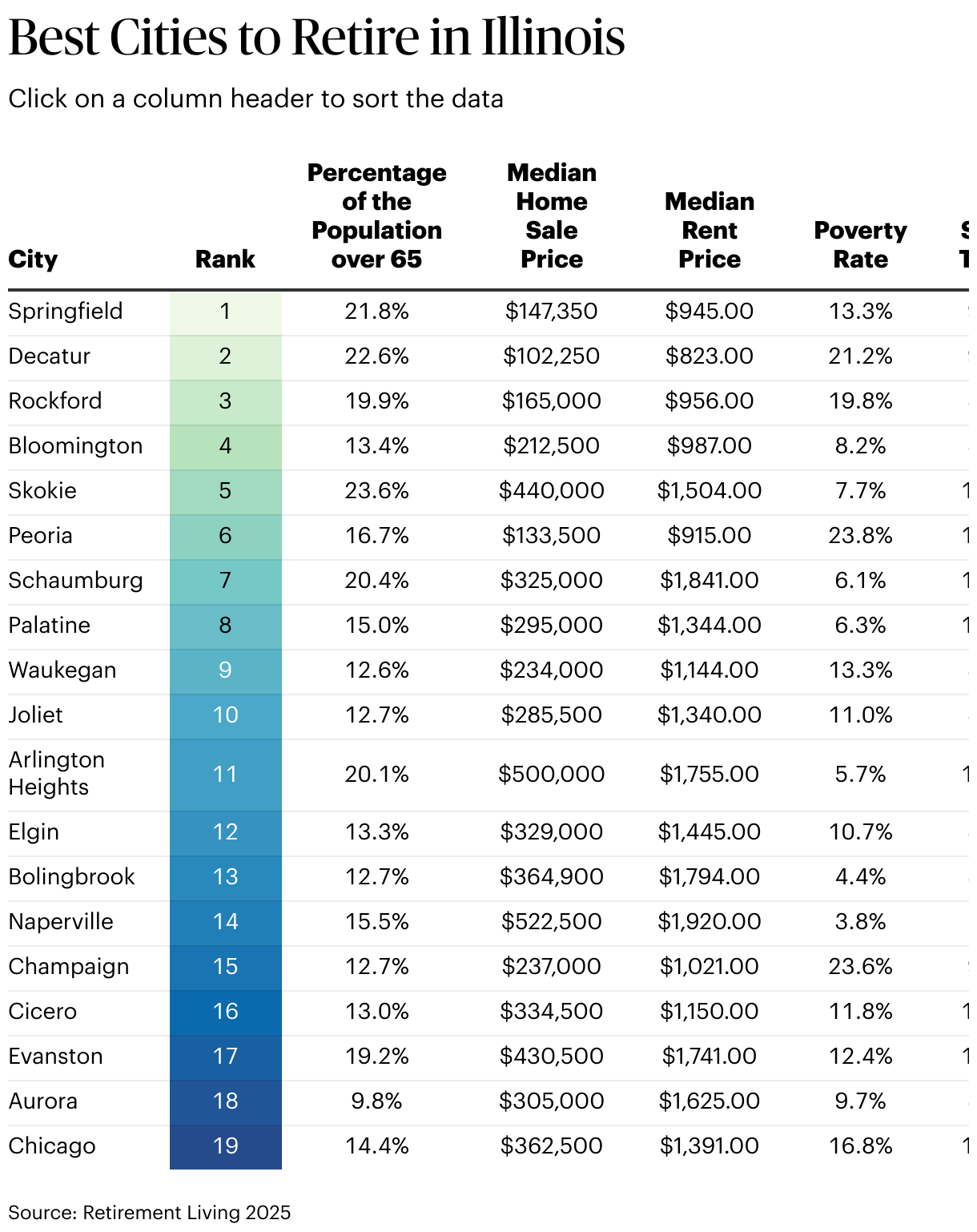

Best Cities to Retire in Illinois in 2025

Best Cities to Retire in Illinois in 2025

Updated:

Open Access

Looking for the perfect city to retire in Illinois? From lively cities to quiet small towns, Illinois offers plenty of options to make you feel at home.

One of the best perks? Illinois doesn’t tax retirement income. Your Social Security benefits, pensions and withdrawals from retirement plans all qualify for full tax deductions. Combined with strong senior communities and a bustling life, Illinois stands out as an appealing and affordable state to retire in.

Key Insights

Springfield ranks as the best city to retire in Illinois due to seniors making up 21.8% of the population and its affordable housing costs.

↓ Jump to insight

Decatur stands out as the most affordable city for retirees, with the lowest median home and rent prices in the state.

↓ Jump to insight

Skokie has the highest share of residents aged 65+ and strong financial stability despite higher housing costs.

↓ Jump to insight

Five top-ranked cities, including Skokie, Schaumburg, and Palatine, fall within the Chicago metro.

↓ Jump to insight

To make your search easier, we pulled together the 10 best cities to retire in Illinois. We compared key factors like the percentage of residents 65+, median home prices, median rent, poverty rates, and sales taxes.

For those considering retirement options beyond Illinois, we recommend exploring our related guides: 10 Best U.S. Cities for Retirement and our breakdown of the Best and Worst States to Retire In.

Top 10 Cities to Retire in Illinois

Here’s how the top 10 cities in Illinois stack up for retirement.

1. Springfield, Illinois

- Share of population 65+: 21.8%

- Median home sale price: $147,350

- Median rent price: $945

- Poverty rate: 13.3%

- Sales tax: 9.75%

Springfield offers that perfect balance, a smaller city with suburban charm that doesn’t sacrifice access to amenities. As Illinois’ state capital, you’ll enjoy shorter commutes, cultural diversity, and pleasant Midwestern summers.

Roughly 21.8% of Springfield residents are 65+, making it one of the most retirement-friendly cities in Illinois. Housing is also affordable, with median home prices around $147,350 and a median rent of $945. That means your retirement savings can go much further here.

While the poverty rate sits at 13.3%, Springfield’s low cost of living and strong senior community make it a top contender for anyone looking to retire in Illinois.

2. Decatur, Illinois

- Share of population 65+: 22.6%

- Median home sale price: $102,250

- Median rent price: $823

- Poverty rate: 21.2%

- Sales tax: 9.25%

Decatur brings an urban vibe to central Illinois, faster-paced than its suburban neighbors but still far from the hustle of a major metro like Chicago. It’s a practical choice for retirees who prioritize socializing and city perks, without the high cost.

The median home price is just $102,250, and the median rent is around $823, one of the most budget-friendly cities in Illinois. The city also has a strong senior presence with 22.6% of residents aged 65+.

That said, Decatur’s poverty rate is 21.2%, the second-highest rate on our list. Financial stability can vary depending on the neighborhood, so it’s worth exploring the area before making a move.

3. Rockford, Illinois

- Share of population 65+: 19.9%

- Median home sale price: $165,000

- Median rent price: $956

- Poverty rate: 19.8%

- Sales tax: 8.75%

If you love spending time outdoors, Rockford could be your spot. With its parks, gardens, and scenic river pathways, there’s no shortage of places to enjoy nature at your own pace.

Rockford has a strong senior presence with 19.9% of its population aged 65+. It’s also one of the more tax-friendly cities, with a sales tax of just 8.75%, helping your day-to-day expenses stay a little more manageable.

The median home price is about $165,000, and the median rent is $956, offering good value compared to some of the pricier cities in Illinois.

One consideration: the city’s poverty rate is 19.8%, which is something to keep in mind when considering long-term financial stability.

4. Bloomington, Illinois

- Share of population 65+: 13.4%

- Median home sale price: $212,500

- Median rent price: $987

- Poverty rate: 8.2%

- Sales tax: 8.75%

Located between Chicago and St. Louis, Bloomington delivers the welcoming atmosphere and relaxed pace many retirees crave after years in fast-paced environments.

Housing in Bloomington remains affordable, with median home prices around $212,500 and the median monthly rent around $987. What truly sets Bloomington apart is its strong economic stability. Its 8.2% poverty rate is among the lowest on our list, suggesting a community where financial well-being is widespread.

Although Bloomington has a lot to offer, only 13.4% of its residents are 65 or older, which is lower than some other cities on our list. We recommend exploring Bloomington’s diverse neighborhoods to find the perfect place that matches your preferred retirement lifestyle.

5. Skokie, Illinois

- Share of population 65+: 23.6%

- Median home sale price: $440,000

- Median rent price: $1,504

- Poverty rate: 7.7%

- Sales tax: 10.25%

Just a stone’s throw from downtown Chicago, Skokie offers that rare combination many retirees dream about, peaceful suburban living with a short drive from city experiences.

Skokie has the highest senior population on our list, with 23.6% of residents aged 65 or older, making connecting with neighbors who may share similar lifestyles or interests easier. A low poverty rate of 7.7% also points to a stable, well-supported city.

However, retiring here comes at a price. The median home price is roughly $440,000, and the median rent is about $1,504, among the highest on our list. Add a 10.25% sales tax, and retirees can expect higher everyday costs, making Skokie a better fit for those with a more flexible retirement budget.

6. Peoria, Illinois

- Share of population 65+: 16.7%

- Median home sale price: $133,500

- Median rent price: $915

- Poverty rate: 23.8%

- Sales tax: 10%

Located along the Illinois River, Peoria combines waterfront views with a rich history that few Illinois cities can match. As one of the state’s oldest settlements, Peoria offers a distinctive character and slow pace that many retirees find refreshing.

Peoria stands out for its affordability, with a median home sale price around $133,500 and a median rent of $915, making it the second most affordable on our list.

It’s worth noting that only 16.7% of the city’s population is 65+, so the senior community here isn’t as large as the others on our list. Retirees should also consider the city’s poverty rate, which is 23.8%, the highest among the cities we analyzed.

7. Schaumburg, Illinois

- Share of population 65+: 20.4%

- Median home sale price: $325,000

- Median rent price: $1,841

- Poverty rate: 6.1%

- Sales tax: 10%

Tucked away in northeastern Illinois, Schaumburg blends small-town comfort with just enough city energy to keep things interesting.

Schaumburg has a strong senior presence, with 20.4% of its residents aged 65 and older. Schaumburg stands out for its financial stability, with the lowest poverty rate at just 6.1%.

However, housing here is on the higher end. The median home price is around $325,000, and the median rent is $1,841. Schaumburg could be an excellent choice for retirees who prioritize a polished environment with great amenities and can plan for the extra cost.

8. Palatine, Illinois

- Share of population 65+: 15%

- Median home sale price: $295,000

- Median rent price: $1,344

- Poverty rate: 6.3%

- Sales tax: 10%

Located in Chicago’s northwest suburbs, Palatine is a favorite for retirees who want an active community with plenty of parks, trails, and events to stay connected.

Financial stability is a significant advantage here. With a poverty rate of just 6.3%, Palatine ranks as the second most financially secure place on our list..

However, affordability is something to consider. Homes typically sell for a median price of $295,000, and the median rent is about $1,344. Combined with a 10% sales tax, your day-to-day expenses could stretch your budget more than you’d like.

9. Waukegan, Illinois

- Share of population 65+: 12.6%

- Median home sale price: $234,000

- Median rent price: $1,144

- Poverty rate: 13.3%

- Sales tax: 8.50%

Sitting along the shores of Lake Michigan, Waukegan offers retirees a waterfront lifestyle that few Illinois cities can match.

Beyond the natural attractions, Waukegan also offers the lowest sales tax on our list at 8.5%, helping to keep everyday costs more manageable.

Housing costs in Waukegan fall in the middle-to-upper range of our list, with median home prices around $234,000 and median rent at $1,144. It’s also worth noting that seniors make up just 12.6% of the population, the lowest on our list, which means you’ll be part of a more age-diverse community.

10. Joliet, Illinois

- Share of population 65+: 12.7%

- Median home sale price: $285,500

- Median rent price: $1,340

- Poverty rate: 11%

- Sales tax: 8.75%

Rich in history dating back to the early 1800s, Joliet offers retirees a unique experience where the past blends in with the present.

Financial security is one of Joliet’s stronger points. With a poverty rate of just 11% and a sales tax of 8.75%, it offers more breathing room for day-to-day expenses compared to other cities in Illinois. Housing costs are also reasonably affordable, with median home prices around $285,500 and a median rent of $1,340.

Seniors make up just 12.7% of the population in Joliet, the second-lowest on our list.

See Where Your Illinois Community Ranks for Retirement

Didn’t see your city? Below is a ranking of the top Illinois cities we compared to find the best places for retirement.

Methodology

We focused on Illinois communities with at least 40,000 residents and compared the factors that matter most for retirement. That includes housing costs, poverty rates, tax burdens, and the percentage of older adults. Each factor was weighted based on how much it impacts everyday retirement life.

For the data, we pulled from trusted, up-to-date sources. Population, rent prices, and poverty rates came from the 2023 American Community Survey (1-Year Estimates). Home sale prices were based on Redfin’s February 2025 data, and sales tax rates came from Avalara.

Here’s how each factor contributed to the overall rankings:

- Percentage of Population 65+: 30%

- Median Home Sale Price: 20%

- Median Monthly Rent: 20%

- Poverty Rate: 20%

- Sales Tax: 10%

Reference policy

If you find this information useful, you can share it for non-commercial purposes. However, we request that you include a link back to this page to give proper credit.

Article sources

- 2023 American Community Survey 1-Year Estimates

- Redfin

- Avalara