Could robots soon care for older adults? We asked the experts

Could robots soon care for older adults? We asked the experts

Technology already exists to help with some tasks

Updated:

Photo by Getty Images on Unsplash

Key Insights

- AI-powered elder care robots are emerging faster than many realize—but full autonomy remains nearly a decade away.

- Experts agree these systems will assist rather than replace human caregivers, handling logistics, monitoring, and companionship.

- The future lies in hybrid care: human empathy supported by robotic precision.

By 2050, one in six people in the world will be over 65, according to the World Health Organization. As the U.S. population ages, the demand for caregiving far outpaces the supply of human professionals. That’s where robotics and AI enter the conversation—not as science fiction, but as an urgent necessity.

“The need for AI-powered solutions for older adults is becoming a global need,” Adrian Dunkley, founder of StarApple AI, told Retirement Living. “Supportive use-cases such as monitoring, reminders, and social interaction are already here. But full-fledged robots that provide physical care like mobility or dressing are nearly a decade away.”

Even though the dream of a fully autonomous elder care robot remains distant, simpler forms are already finding their way into homes and care facilities. These devices track vital signs, detect falls, and even chat with users.

“All of the technology already exists,” explains Bob Hutchins, CEO of Human Voice Media. “Robots can already remind a person to take their medicine, monitor vital signs, and use primitive natural language processing to offer at least a facsimile of companionship.”

But Hutchins cautions that the word care might be misleading. “Care is more than simple protocols or routines. It’s reading the emotional temperature of a person in real time. A robot can run a script. It can’t tell when someone is frightened, lonely, or confused.”

In other words, the machines are getting smarter, but they’re not yet sensitive.

“Then there’s the entire mobility aspect,” said Michael Nielson, vice president of marketing at RealSense. “Robotics could be a game changer for preventing falls on walkers, assisting automated wheelchairs – even with navigation, and even with assisted loading of disabled patients into vans.”

Four pillars of robotic assistance

Dunkley divides robotic elder care into four main categories:

- Monitoring and safety — AI systems that track falls, vital signs, and behavioral changes.

- Social interaction — Companion bots like ElliQ that engage seniors in conversation.

- Personalization and adaptation — Systems that learn routines and preferences to tailor care.

- Assistive physical support — The ultimate goal: robots capable of mobility aid and physical assistance.

The first three are here today, but that last one – the physical, adaptive caregiver – remains the “holy grail.” As Dunkley notes, “Boston Dynamics’ Atlas android is capable of amazing feats of dexterity and strength, but can’t hold a candle to the intuition of a seasoned caregiver.”

The role of AI and human synergy

While some see robots as potential replacements for human caregivers, others envision them as partners. Leury Pichardo, marketing director at Digital Ceuticals, describes the future of elder care as a collaboration between AI and people.

“The goal isn’t to build a machine with empathy,” he says. “It’s to build a machine that handles all the administrative noise so the human can focus entirely on providing empathy and connection.”

Pichardo imagines AI assistants managing logistics – scheduling appointments, reordering prescriptions, and tracking daily movement – “absorbing the 80% of logistical work that burns caregivers out.”

The path to commercial adoption

According to Ishraq Khan, a startup founder building intelligent systems, “We are closer than most people realize. The mechanical and sensor technology is already well developed, but the intelligence layer has lagged behind.”

Khan predicts pilot programs will begin within two years, especially in Asia and Europe, with U.S. commercialization around 2028.

“We’re about three to five years from semi-autonomous elder care robots operating safely under supervision, and eight to ten years from fully autonomous systems,” he told us.

That timeline aligns with Dunkley’s estimate of mainstream adoption within five to 10 years, depending on regulation, trust, and cost. Hutchins remains more cautious, emphasizing that technology alone isn’t the limiting factor.

“The real question is whether we’re deploying these tools because they measurably increase quality of life, or because we’ve decided human caregivers are too expensive,” he said. That’s a political choice, not a technology problem.”

A human future with robotic help

The consensus among experts is clear: robots won’t replace empathy. They’ll amplify it. AI may soon handle reminders, scheduling, and even mobility, but the heart of elder care will always remain human.

As Dunkley puts it, “The technology is evolving rapidly, but large-scale adoption in elder-care homes and private homes remains a future milestone.”

That future, while not quite here, is coming faster than most people think—and it might just help us care for our loved ones longer, safer, and with more dignity.

Most people ignore a powerful retirement tool: The Roth 401(k)

Most people ignore a powerful retirement tool: The Roth 401(k)

A report from Vanguard found 80% of employers offer one

Updated:

Photo by Getty Images on Unsplash

Key Insights

- More than 85% of employers offer a Roth 401(k) option, but fewer than 20% of workers use it.

- A Roth 401(k) allows for tax-free withdrawals in retirement, unlike traditional 401(k) accounts.

- Choosing a Roth 401(k) can provide greater tax flexibility and help manage costs in retirement.

If your employer offers a retirement plan, chances are you have access to one of the best savings options available, but most people aren’t taking advantage of it.

According to new data from Vanguard, more than 85% of 401(k) plans include the option to contribute to a Roth 401(k). Yet fewer than one in five employees who have this choice are using it.

That gap has financial experts puzzled. During the annual open enrollment period, when workers review and update their benefits for the coming year, many may be missing an opportunity to set themselves up for more tax-efficient retirement income.

What makes a Roth 401(k) different

The key difference between a Traditional 401(k) and a Roth 401(k) comes down to when you pay taxes.

- With a Traditional 401(k), contributions reduce your taxable income in the year you make them. For instance, if you earn $85,000 and contribute $10,000, you’re taxed as though you earned $75,000. However, withdrawals in retirement are fully taxable, and you’ll eventually be required to take distributions starting at age 73 (for those born between 1951 and 1959) or 75 (for those born in 1960 or later).

- With a Roth 401(k), contributions are made with after-tax dollars. That means you don’t get an upfront tax break, but once you retire, your withdrawals—including all investment gains—are completely tax-free. There’s also no required minimum distribution, so your money can stay invested as long as you like.

Why Roth contributions can pay off later

Financial planners increasingly recommend diversifying retirement savings between pre-tax and after-tax accounts. For workers who have long contributed to a Traditional 401(k), shifting new contributions to a Roth 401(k) starting in 2026 could offer long-term benefits.

Tax-free income in retirement can help keep your overall taxable income lower, potentially reducing Medicare Part B premiums and even limiting the taxes owed on Social Security benefits. It also provides more flexibility to manage your income from year to year, depending on your needs and the tax environment.

While a Traditional 401(k) remains a solid retirement tool, adding Roth savings – through either a Roth 401(k) or a Roth IRA – can be a smart way to build financial flexibility for the future. As open enrollment season approaches, now is an ideal time for employees to review their plan options and consider making the switch.

According to personal finance expert Suze Orman, the Roth 401(k) may be the best retirement benefit you’re not using.

Most women don’t seek medical care for menopause symptoms

Most women don’t seek medical care for menopause symptoms

Mayo Clinic survey finds menopause ‘under‐recognized and undertreated’

Updated:

Photo by Molly Wichman on Unsplash

Key Insights

- A new study by Mayo Clinic finds that more than 75% of women aged 45-60 who reported menopause symptoms had not sought medical care for them.

- Among the nearly 5,000 women surveyed, 34% reported moderate to very severe symptoms, including sleep disturbances and weight gain — yet only about 25% were receiving any treatment.

- Researchers call for better screening tools, digital apps and proactive engagement by healthcare providers to address what they describe as a major treatment gap in midlife women’s health.

While the transition through menopause is nearly universal for midlife women, a newly published study from the Mayo Clinic reveals a striking disconnect: the majority of women experiencing menopause-related symptoms are navigating this life stage without seeking medical support.

The study, published in the journal Mayo Clinic Proceedings, surveyed nearly 5,000 women between ages 45 and 60 across four Mayo Clinic primary-care sites. It found that over three-quarters of those women reported experiencing symptoms associated with menopause.

Despite the frequency of symptoms and the availability of “safe and effective treatment options”, the researchers conclude that menopause symptoms remain “under‐recognized, undertreated and inadequately addressed in the health-care system.”

Significant symptom burden, limited care

Of particular concern: 34% of respondents reported their symptoms as moderate to very severe. The most commonly reported issues were sleep disturbances and weight gain — each cited by more than half of participants.

Yet, more than 80% of the women in the survey had not sought medical care for their menopause symptoms. Many said they preferred to manage symptoms on their own; others cited being too busy or unaware that effective treatments existed. Meanwhile, only about one in four were receiving any form of treatment at the time of the survey.

“Menopause is universal for women at midlife, the symptoms are common and disruptive, and yet, few women are receiving care that could help them,” said lead author Dr. Ekta Kapoor, an endocrinologist and menopause specialist at the Mayo Clinic. She emphasized that the care gap has “real consequences for women’s health and quality of life.”

Implications for quality of life

The study highlights that untreated menopause symptoms can negatively affect sleep, mood, cognition and productivity — both at work and at home.

Because of this, the Mayo Clinic team said healthcare providers should more proactively screen for menopause symptoms and engage patients in discussions about management options — rather than waiting for women to raise the issue themselves.

For women experiencing sleep issues, weight changes, mood shifts or other midlife symptoms, the study suggests benefit in initiating a conversation with their healthcare provider — even if they’ve assumed the symptoms are simply “part of life.”

Three reasons your utility bills are rising this year

Three reasons your utility bills are rising this year

The good news? There are things you can do about it

Updated:

Photo by Ian Noble on Unsplash

Key Insights

- Higher fuel and infrastructure costs are driving up electricity and gas prices nationwide.

- Extreme weather and aging grids are forcing utilities to invest heavily in upgrades and repairs.

- Consumers can offset rising bills through energy efficiency, smart usage habits, and new incentive programs.

Living on a fixed income can be a challenge, especially when everyday expenses go up unexpectedly. So, retirees may want to prepare now – utility bills are expected to keep rising well into 2026.

The reason isn’t simple. It’s a combination of economic pressures, infrastructure challenges, and climate realities that are reshaping how utilities deliver power.

For starters, utilities are paying higher costs for the fuels that generate most of America’s electricity — natural gas, coal, and oil – and those costs usually get passed on to consumers.

Global demand for energy remains strong, and geopolitical tensions have disrupted supply chains. Even as renewable energy grows, the U.S. grid still relies heavily on natural gas plants to meet daily demand. When the cost of fuel rises, those increases often get passed along to consumers through rate adjustments approved by state regulators.

Extreme weather

There are increasing pressures on the grid. Extreme weather — from hurricanes and wildfires to heat waves — is battering energy infrastructure nearly every year. Utilities are responding by investing billions in grid modernization: hardening power lines, building new substations, and improving energy storage. These upgrades are necessary to prevent outages and maintain reliability, but they also drive up operational costs that end up on consumer bills.

Finally, inflation has affected everything from the cost of transformers and copper wire to labor and transportation. Construction and maintenance projects that once cost millions now require much more funding. Since utilities operate under regulated profit structures, they typically seek permission from state utility commissions to raise rates and recover those costs over time.

What consumers can do

While no single household can reverse national energy trends, there are many ways to ease the impact, broken down by energy type.

Electric bills

- Switch to LED lighting

LEDs use up to 80% less energy and last longer than incandescent bulbs. - Unplug “energy vampires”

Devices like TVs, chargers, and game consoles draw power even when off. Use smart power strips to cut phantom loads. - Use smart thermostats

A programmable thermostat can save 10–15% on heating and cooling by adjusting temperatures automatically. - Run appliances efficiently

- Wash clothes in cold water.

- Run full loads in the dishwasher and washing machine.

- Air-dry clothes when possible.

- Seal and insulate your home

Proper insulation and sealing leaks around windows and doors can reduce heating/cooling bills significantly.

Conserve water

- Install low-flow fixtures

Low-flow showerheads and faucets cut water use without sacrificing pressure. - Fix leaks promptly

Even a small drip can waste hundreds of gallons of water per year. - Use efficient appliances

ENERGY STAR-rated dishwashers and washing machines use less water and energy. - Collect rainwater or use gray water for outdoor irrigation.

Heating and cooling efficiency

- Maintain your HVAC system

Clean filters monthly and schedule annual tune-ups to improve efficiency. - Use ceiling fans

Fans help circulate air—set them to spin counterclockwise in summer and clockwise in winter. - Close unused vents and doors

Focus heating and cooling only on occupied areas. - Weatherize windows

Add thermal curtains or window film to prevent heat loss in winter and block sunlight in summer.

Long-term upgrades

- Install solar panels or community solar participation

Depending on your region, this can reduce or eliminate electricity bills over time. - Upgrade to energy-efficient appliances

When old ones wear out, replace them with ENERGY STAR-rated models. - Consider home energy audits

Utilities often offer free or discounted audits to identify where you can save.

Smart habits

- Turn off lights when leaving a room.

- Cook with lids on pots and match pot size to burner size.

- Lower your water heater temperature to 120°F (49°C).

- Track energy use with apps or smart meters to spot waste patterns.

Untreated hearing loss may increase the risk of dementia

Untreated hearing loss may increase the risk of dementia

Study finds hearing aids reduce the risk of cognitive decline

Updated:

Photo by Curated Lifestyle on Unsplash

Key Insights

- A new study published in JAMA finds that older adults with untreated hearing loss face a significantly higher risk of developing dementia.

- Hearing aid use was linked to slower cognitive decline, suggesting treatment can help protect brain health.

- Researchers emphasize early detection and hearing care as key steps in preventing dementia.

Hearing loss can be a normal part of aging. But a new study published in the Journal of the American Medical Association (JAMA) adds to growing evidence that untreated hearing loss is more than an inconvenience — it’s a serious risk factor for dementia.

The research, which followed thousands of older adults for several years, found that people with untreated hearing loss were up to twice as likely to develop dementia compared with those who maintained normal hearing. Even more striking: those who used hearing aids had a significantly lower risk of cognitive decline.

“These findings reinforce that hearing care is brain care,” the study authors wrote. “Addressing hearing loss may be one of the most effective, accessible ways to reduce dementia risk in aging adults.”similar to an IRA—so there’s no penalty if you decide to use the funds for general retirement expenses.

The study behind the findings

Researchers analyzed data from a large cohort of adults aged 60 and older, tracking hearing levels, hearing aid use, and cognitive performance over time. Participants underwent routine cognitive assessments that measured memory, attention, and executive function.

The results showed a clear pattern:

- Untreated hearing loss was associated with accelerated cognitive decline and higher dementia incidence.

- Hearing aid users, however, experienced cognitive decline rates similar to peers with normal hearing.

This protective effect was strongest among older adults who had significant hearing loss at baseline but began using hearing aids early in the study period.

Why hearing affects the brain

Experts believe the connection between hearing and cognition is multifaceted:

- Cognitive load: When the brain has to work harder to interpret sound, fewer resources are left for memory and thinking.

- Social isolation: Hearing loss can lead to withdrawal and loneliness — both linked to dementia.

- Brain structure changes: MRI studies show that untreated hearing loss can cause shrinkage in areas of the brain responsible for sound and comprehension.

“People often dismiss hearing loss as a normal part of aging,” said one researcher, “but this study shows that leaving it untreated may actually accelerate brain aging.”

Hearing aids could be a protective tool

The study’s authors highlight that hearing aids are more than just devices to improve communication — they may act as a protective tool for long-term brain health. Yet, fewer than 1 in 5 adults who could benefit from hearing aids actually use them.

Newer over-the-counter hearing aids, approved by the FDA in recent years, are making treatment more affordable and accessible. Experts encourage anyone struggling to follow conversations — especially in noisy settings — to get a hearing test as part of routine health care.

What consumers can do

The message for consumers is simple: Don’t ignore hearing loss.

- Get your hearing tested regularly, especially after age 50.

- Treat hearing loss early. Hearing aids or other interventions may help preserve brain health.

- Stay socially and mentally active. Engaging with others, exercising, and keeping the mind stimulated can reduce dementia risk.

“Addressing hearing loss isn’t just about improving quality of life,” the researchers concluded. “It’s a step toward protecting your mind for years to come.”

How retirees can invest unused HSA funds to grow the account

How retirees can invest unused HSA funds to grow the account

Here’s how to turn health savings into wealth savings

Updated:

Photo by Getty Images on Unsplash

Key Insights

- Unused money in a Health Savings Account (HSA) can be invested for long-term growth.

- HSAs offer triple tax advantages—contributions, growth, and withdrawals for qualified expenses are all tax-free.

- Strategic investing within an HSA can help cover future medical costs or even serve as a supplemental retirement fund.

Many retirees leave their Health Savings Accounts idle, assuming the funds should only be used for medical bills. But HSAs can do far more than that—they can become powerful investment tools.

Unlike Flexible Spending Accounts (FSAs), HSAs don’t expire, meaning your money can stay invested and continue to grow, tax-free, year after year.

HSAs stand out for offering three layers of tax benefits:

- Contributions are tax-deductible. Even if you’re retired, you can still contribute to an HSA if you have a high-deductible health plan.

- Earnings grow tax-free. Any interest, dividends, or capital gains generated from investments inside the HSA aren’t taxed.

- Withdrawals for qualified expenses are tax-free. That includes everything from prescriptions to long-term care premiums.

After age 65, withdrawals for non-medical purposes are taxed like regular income—similar to an IRA—so there’s no penalty if you decide to use the funds for general retirement expenses.

Investment options inside an HSA

Many HSA providers allow you to invest in mutual funds, ETFs, or other securities once your account balance reaches a minimum threshold (often around $1,000–$2,000). You can build a diversified portfolio tailored to your risk tolerance and time horizon.

For example, a retiree might:

- Keep a portion in cash or short-term bonds for upcoming medical expenses.

- Invest the remainder in broad-based index funds for long-term growth.

“The plan is to go into retirement with a six-figure HSA,” certified financial planner Dan Galli, owner of Daniel J. Galli & Associates in Norwell, Massachusetts, told CNBC. When coupled with other Roth and after-tax retirement funds, “this is the holy grail of retirement planning,” he said.

As healthcare costs continue to rise, investing unused HSA funds can help create a financial cushion for future medical needs, or even reduce your dependence on other retirement accounts. It’s a flexible strategy that keeps your money working for you, well into your later years.

Before making any changes, consult with a financial advisor or tax professional to ensure your HSA investments align with your overall retirement plan.

Retired investors prefer steady income over maximizing returns

Retired investors prefer steady income over maximizing returns

But financial advisors see that as too conservative, survey finds

Updated:

Photo by Getty Images on Unsplash

Key Insights

- Capital Group surveyed more than 5,000 investors spanning different life stages, asking how they are approaching investing for retirement income.

- The survey showed investors are willing to sacrifice higher investment returns in exchange for steady income.

- Investors also showed a preference for preserving 100% of their retirement savings, even if it meant accepting a lower level of retirement income.

For many Americans planning or living in retirement, the old adage, “a bird in the hand is worth two in the bush,” seems to apply. According to a new Capital Group Investor Retirement Income Survey, retirees and pre-retirees overwhelmingly prefer steady income and capital preservation over chasing higher returns.

The survey of more than 5,000 investors found that nearly six in ten (59%) would accept lower returns if it meant lowering investment risk — a reflection of a growing appetite for stability in an uncertain economic climate.

“The survey shows investors are risk-averse in retirement planning across a number of areas,” said Samir Mathur, portfolio manager and member of Capital Group’s Capital Solutions Group. “When it comes to retirement income, people prefer lower risk and steady income over higher risk and the potential for higher returns.”

Risk aversion increases with age

As retirement nears, financial caution increases. The survey found that 78% of retirees preferred lower-risk options, compared with 54% of investors further from retirement. Many are also holding a substantial share of their portfolios — about 41% on average — in “low-risk” assets such as bonds or cash equivalents.

Even when offered the chance to grow their savings by 50%, few investors said they’d risk losing more than 15% of their nest egg. Inflation worries, market volatility, and lingering economic uncertainty may all play a part in this conservative stance.

Perhaps the most striking finding: investors’ desire to preserve 100% of their savings during retirement, even while taking withdrawals. This goal may not be entirely realistic, but it underscores a deep emotional and psychological connection to the retirement nest egg — one that’s stronger among older investors and those with higher assets.

“People want to feel their lifetime of saving won’t disappear,” said Mathur. “Even if that means accepting a smaller paycheck in retirement.”

How retirees fund their ‘paycheck’

The survey revealed generational differences in how retirees expect to fund their living expenses:

- Retirees today rely heavily on Social Security (46%), followed by employer-sponsored savings plans and personal investments.

- Younger investors expect those roles to reverse — with 401(k)s and similar accounts playing a bigger part as Social Security’s future feels uncertain.

At the same time, 76% of respondents said they are willing to tap into their principal if needed, showing that while many want to preserve capital, practicality often wins when expenses arise.

When asked to choose a time horizon for withdrawals, most investors favored a 20-year plan, even though 70% believe their savings will last longer. However, a growing share is shifting toward 30-year horizons, likely reflecting longer life expectancies and better investment conditions, such as higher bond yields.

Advisors, meanwhile, take a different view. Capital Group’s companion survey of financial professionals found that advisors are more tolerant of risk, willing to weather up to a 30% decline in account balances and preferring 30-year withdrawal strategies. The contrast highlights a persistent gap between professional guidance and investor comfort levels.

Despite their caution, retirees and near-retirees aren’t pessimistic. Roughly 69% of investors said they feel confident they will meet their retirement goals — a sign that prudence and optimism can coexist.

In short, today’s retirees appear to be redefining success in retirement. Instead of maximizing returns, they’re focused on maximizing peace of mind — opting for predictability, stability, and the reassurance that their savings will last as long as they do.

Music may help keep aging brains sharp, study finds

Music may help keep aging brains sharp, study finds

This could be good news for a generation that grew up listening to tunes

Updated:

Photo by Vitaly Gariev on Unsplash

Key Insights

- Listening to music regularly can lower dementia risk by nearly 40% in older adults.

- Playing an instrument may reduce dementia risk by about 35%.

- Combining music listening and playing offers added protection for cognitive health.

Baby boomers loved their music in their youth, from Marvin Gaye to the Beatles. A new study suggests boomers should continue to embrace their favorite tunes.

A new study led by researchers at Monash University has found that older adults who regularly listen to music enjoy significant protection against dementia, with up to a 39% lower risk compared to those who rarely tune in. The research, published in the International Journal of Geriatric Psychiatry, analyzed data from more than 10,800 participants aged 70 and older in the ASPREE and ALSOP studies.

The study, led by honors student Emma Jaffa and Professor Joanne Ryan, revealed that those who “always” listened to music had the greatest reduction in dementia risk, along with a 17% lower incidence of cognitive impairment.

These participants also performed better in overall cognition and episodic memory, which helps people recall everyday events and experiences.

Playing an instrument provided similar benefits, with a 35% lower risk of dementia. Even better, seniors who both listened to and played music regularly saw a 33% lower risk of dementia and a 22% lower risk of cognitive impairment.

Why it matters

As the global population ages, dementia has become a growing public health concern. While advances in medicine and technology have extended life expectancy, age-related conditions such as cognitive decline are also on the rise. With no current cure for dementia, preventive strategies are increasingly vital.

“This study suggests music activities may be an accessible strategy for maintaining cognitive health in older adults,” said Jaffa. “Though causation cannot be established, the link between music and brain health is compelling.”

Ryan added that brain aging isn’t determined by age or genetics alone. “Our study suggests that lifestyle-based interventions, such as listening to or playing music, can promote cognitive health,” she said.

For seniors looking for an easy, enjoyable way to support brain health, the message is clear: keep the music playing. Whether it’s singing along to favorite tunes, strumming a guitar, or simply relaxing to classical pieces, engaging with music could help preserve memory and mental clarity well into later life.

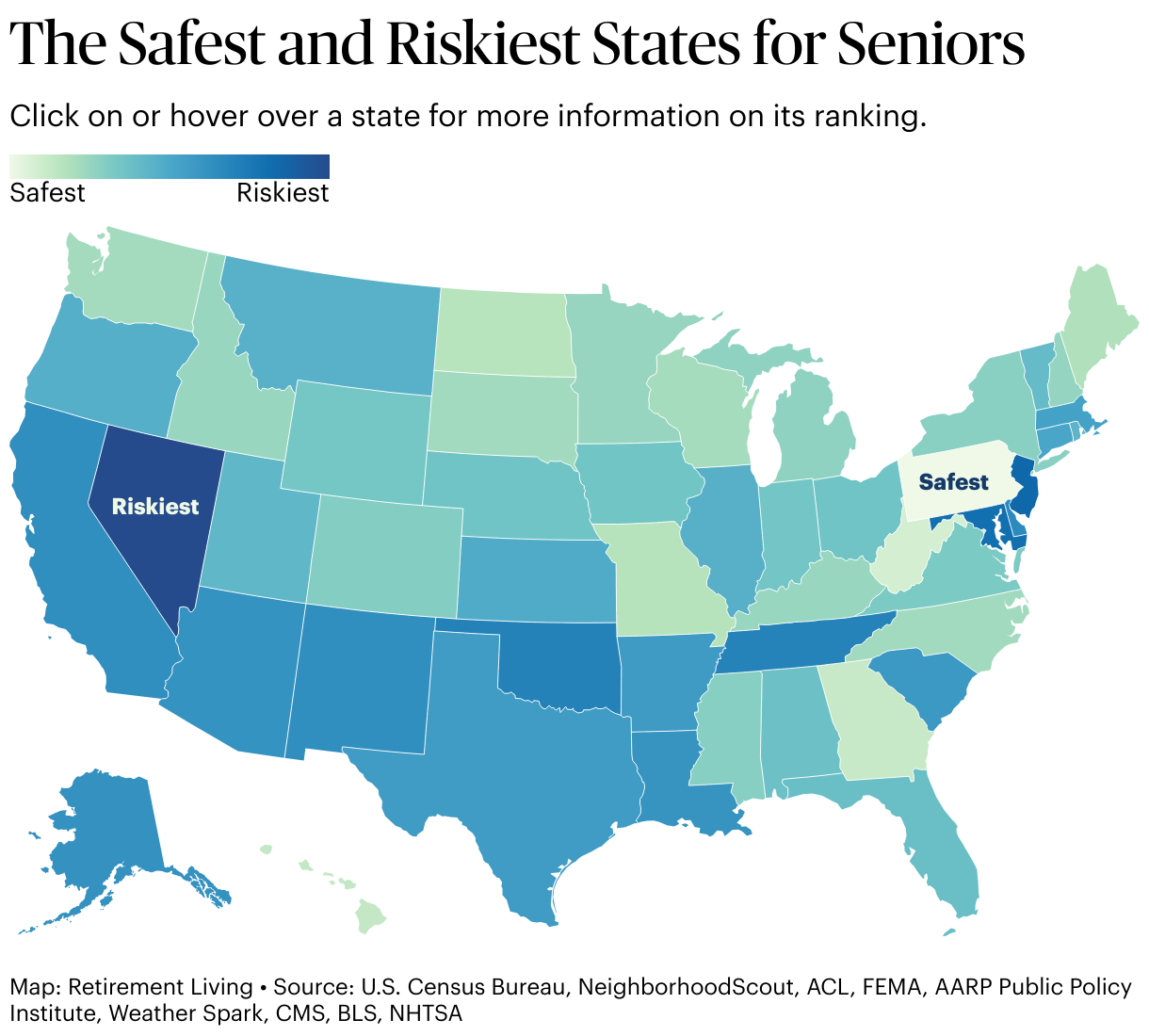

The Safest and Riskiest States for Seniors

The Safest and Riskiest States for Seniors

Updated:

Open Access

America is aging rapidly, with the 65-and-over population growing five times faster than the total population. Seniors are also one of the country’s most vulnerable populations, facing greater risks from crime, climate, health emergencies, and more. While these issues present dangers to seniors everywhere, just how much risk they present varies from place to place.

Key Insights

Pennsylvania is the country’s safest state for seniors, largely due to low crime rates and limited climate risk.

↓ Jump to insight

Nevada is the riskiest state in the U.S. for seniors, with some of the country’s hottest temperatures in summer and the highest rate of elder abuse.

↓ Jump to insight

Only nine U.S. states currently have an enhanced state hazard mitigation plan in place.

↓ Jump to insight

Maryland ranks as the worst state for senior health care access.

↓ Jump to insight

Every region is represented in the 10 safest states for seniors in the country; the Midwest and South each lead with three.

↓ Jump to insight

Choosing where to spend your retirement is about more than affordability. It’s also about finding a place to live that is safe and secure and offers ample access to quality health care. With tens of millions of Americans now considering how and where to spend their golden years, we created this guide to help identify which states are the safest for retirees and highlight the risks to seniors in each one.

The Five Safest States for Seniors

Our senior care report provides a clear look at how each state supports its aging population. Ranks are calculated using 17 weighted factors, measuring healthcare quality, access, community support, and overall senior living conditions. Whether you’re planning a cross-country move or staying in your current home, the key is matching your personal priorities with what each state offers best.

1. Pennsylvania

The safest state for seniors in our 2025 study is Pennsylvania, which earned top 20 safety scores in all but one major category. Pennsylvania performed especially well in two categories in particular: crime and climate.

Elder abuse is relatively uncommon in Pennsylvania, which sees just 7.5 reported incidents per 100,000 seniors in the state. The Keystone State ranks fourth overall in climate safety, thanks to moderate temperatures throughout the year. Pennsylvania’s enhanced state hazard mitigation plan ensures that if extreme climate events impact state residents, a Federal Emergency Management Agency-approved plan is in place to minimize the damage. That should provide plenty of peace of mind for senior citizens looking for a secure, comfortable place to retire.

In addition to being a safe place to spend your golden years, Pennsylvania is relatively close to several major metropolitan areas, like New York City. That means seniors can enjoy the peace and serenity the state has to offer while having easy access to big city excitement when the mood strikes.

2. West Virginia

West Virginia claims second place on our list of the safest states for seniors this year with high scores in all but the traffic category, where it ranks 27th. Seniors have relatively little violent crime to worry about in the Mountain State, which has the ninth-lowest violent crime rate in the country, at just 12.4 reported incidents per 1,000 seniors. Property crime is also notably low in West Virginia, with a reported incident rate of 55.6 per 1,000 seniors, the fourth-lowest rate in the nation.

Despite West Virginia’s mostly rural setting, health care access is one of its main strengths. The state ranks within the top 10 for high-quality home health, with more than a quarter (25.5%) of agencies rated 4 stars or above.

West Virginia may be “wild and wonderful,” but our data shows that it’s also safe and comfortable for retirees. The fresh mountain air and beautiful vistas are a big bonus.

3. Georgia

Georgia ranks third overall for the safest states for seniors and is one of two Southern states in the top three. The Peach State excels when it comes to climate safety, ranking fifth overall in the category. Its exceptionally mild winters are the main draw, with an average winter low of a crisp-but-comfortable 41 degrees Fahrenheit. That helps reduce the risk of exposure-related illnesses compared with places that experience consistent freezing temperatures. Georgia also earns points for its relatively low climate risk score from FEMA and for having an enhanced state hazard mitigation plan in place.

While Georgia’s performance in the health care access category is somewhat uneven, it has a few big green flags. The state ranks 11th in lowest average Medicare payments for hospital outpatient services per capita and eighth in the percentage of Medicare recipients enrolled in Medicare Advantage plans.

With mountains in the northern part of the state and gorgeous beaches along its coastline, Georgia is a dynamic state with plenty to offer seniors looking for a little variety in retirement. Our research indicates it’s also a low-risk place for them to make a home.

4. Hawaii

Hawaii would be an attractive retirement destination even if it didn’t earn strong scores for senior safety. In fact, the Aloha State scores high in every major safety category except climate, where it finishes in the middle of all states.

Crime isn’t something retired residents of Hawaii need to worry about much. The state has the fifth-lowest rates of violent crimes (8.9 reported incidents per 1,000 seniors) and elder abuse (3.3 reported incidents per 100,000 seniors) in the country. Seniors have even less to worry about when it comes to cold weather in Hawaii, which has an average winter low temperature of 66, well within the comfort range.

There are a whole lot of reasons for seniors to say “aloha” (goodbye) to the continental U.S. and “aloha” (hello) to Hawaii for retirement. Incredible nature, pristine beaches and a laid-back island lifestyle don’t need data to back them up. The data does, however, confirm the relative safety of moving to Hawaii for one’s golden years.

5. North Dakota

North Dakota closes out our list of the top five safest states for seniors in 2025. In the health care access category, it ranks first in average time spent in the hospital emergency room before going home, at one hour and 50 minutes per visit, the lowest in the country.

While North Dakota ranks second in the nation for overall climate safety and has one of the lowest climate risk scores, retirees should be prepared for its frigid winters. The state’s average low winter temperature is just 7, the coldest in the U.S., even colder than Alaska’s. However, if a natural disaster does occur, North Dakota’s hazard mitigation plan ensures a FEMA-approved response is in place.

North Dakota may not be at the top of most people’s lists when they begin looking for a state to retire in. However, when you combine the relative safety seniors experience while living there with its abundance of natural beauty, perhaps it should be — especially for those who embrace the winter.

What Are The Riskiest States for Seniors?

On the other end of the spectrum are the states that are the least safe for seniors. The following states emerged as the overall riskiest for senior living based on the same criteria used to determine the safest. Each of these states earned an overall senior safety score below the U.S. average, including low scores across multiple evaluation categories.

1. Nevada

Based on our research, Nevada is the riskiest state in the U.S. for seniors to call home. Crime is a major concern in Nevada; it has the fifth-highest rate of property crime, with about 145 incidents per 1,000 seniors. Elder abuse is especially worrisome, with 247.6 reported incidents per 100,000 seniors — the worst in the country. These two crime rates, plus an above-average violent crime rate, make Nevada rank dead last in the crime category.

Climate is also a serious concern for seniors in Nevada. The average summer high temperature of 92 is the third highest of any state, posing a significant risk of heat stroke and other exposure-related illnesses. Winters can also be a problem, with an average low temperature of 28.

Nevada is home to plenty of fun and is conveniently close to many attractions. It’s just not a state that offers much safety and security to residents in their retirement years. For seniors, Nevada is likely a much better place to visit than to call home.

2. New Jersey

New Jersey scores poorly particularly in climate safety and crime, making it the second-riskiest state for seniors. Because the state is vulnerable to hurricanes and other tropical storms during the summer and significant snowfall during the winter, seniors face climate-related risks all year long. This is supported by New Jersey’s climate risk score of 90.2 out of 100, which is the second-highest score of any state in the country.

Rates of violent and property crime are actually below the U.S. averages. However, New Jersey has the second-highest rate of elder abuse of any state, at 239.1 reported incidents per 100,000 seniors.

Despite its reputation, many parts of New Jersey are beautiful, with lush countryside and lots of lovely beaches. The state’s proximity to New York City and Philadelphia can make it an enticing option for seniors who want easy access to city life. That said, seniors who also seek security in retirement have many better options than New Jersey.

3. Maryland

Maryland is the third-riskiest state in the country for seniors, according to our research. It scores in the bottom 15 in every category except traffic safety. The Free State has one of the 10 highest climate risk scores in the U.S., meaning seniors face a strong probability of being affected by severe events. With no enhanced state hazard mitigation plan in place, there’s not as much assurance that seniors will get timely relief and support when disasters happen.

However, the biggest concern for seniors in Maryland is access to health care, with the state ranking last in the country in that category. Maryland has a below-average ratio of home health care workers to seniors, at 36.1 aides for every 1,000 seniors. The state also has the longest ER times in the U.S., at an astounding average of four hours and 11 minutes per visit.

Maryland offers quick access to cities like Washington, D.C., Baltimore and Philadelphia, and is home to a strong local culture and diverse landscapes. Still, it has several red flags for seniors hoping to retire somewhere they can feel secure.

4. Oklahoma

Oklahoma has many points of concern for senior living. While the Sooner State finished in the top half of states for health care access, it ranks poorly in every other category, particularly crime. Oklahoma residents face some of the country’s highest rates of violent and property crimes, as well as the fifth-highest rate of elder abuse of any state, at 88.2 reported events per 100,000 seniors.

Traffic safety is also a significant problem in Oklahoma. It has the fourth-worst traffic safety score, with high rates of fatal crashes and traffic-related deaths involving seniors. Given that public transportation options are limited in this mostly rural state, driving in Oklahoma is both a necessity and a risk for retirees.

5. Tennessee

Closing out our list of the five riskiest states for seniors is Tennessee. Crime is a major factor in the Volunteer State’s below-average score for senior safety. Seniors there are subject to the country’s fourth-highest rate of elder abuse, as well as the eighth-highest rate of property crime. And with a rate of 35.9 reported incidents per 1,000 seniors, Tennessee has the third-highest violent crime rate in the U.S.

Like in Oklahoma, traffic safety is a major concern for Tennessee’s senior residents. The state ranks among the 10 worst in the country for senior-involved fatal crashes and senior traffic fatalities.

Tennessee is loaded with natural sites and theme parks to explore, as well as exciting, culturally important cities to take in. Unfortunately, it doesn’t provide much in the way of safe and secure living for seniors.

How Does Your State Rank for Senior Safety?

Every state has some degree of risk for older adults, with some states less safe than others. The table below lists the overall risk score and category rankings for each state in the U.S. You can use it to see the biggest risks for seniors in your state — or in any others you may be considering for retirement.

Ways to Protect Your Health and Safety in Retirement

The relative threat of crime, climate disasters, low health care access, and deadly traffic may vary throughout the country, but there is no place in the U.S. where seniors are completely free of danger. No matter where you choose to spend your retirement, there are some things you can do to set up guardrails and reduce risks to your health and safety, including:

- Install safety features in your home. Equipment like grab bars in bathrooms and additional handrails on staircases and walkways helps prevent falls and is relatively inexpensive.

- Wear a medical alert device. Bracelets and other medical alert wearables can help ensure you get assistance as quickly as possible if you fall or suffer an accident and can’t reach the phone, when every minute can make a difference.

- Improve your home’s lighting. Installing brighter lights and ensuring all of your home’s pathways and areas of activity are sufficiently lit can reduce the chance of a misstep or running into furniture while moving around.

- Invest in a home security system. An alarm system and other home security tools make your home more difficult to break into and a less appealing target for thieves. Many home security companies offer monitoring services that can get help to your home when you can’t make the call yourself.

- Have a home generator installed. Extreme heat and freezing temperatures pose significant risks for seniors in their homes. A backup generator can ensure that your HVAC system continues to work during power outages and keeps your home at a safe and comfortable temperature.

Methodology

The Retirement Living Research Team identified the safest and riskiest states for seniors by comparing all 50 U.S. states across four weighted categories worth a total of 100 points.

- Crime (35 points): The crime score includes violent and property crime rates per 1,000 seniors (10 points each) and reports of elder abuse per 100,000 seniors (15 points). Data is from NeighborhoodScout (2023) and the Administration for Community Living (2024).

- Climate safety (30 points): The climate safety score factors in a climate risk index score from FEMA (10 points), whether the state has a FEMA-approved enhanced state hazard mitigation plan (10 points) and how far the average summer high and winter low temperatures deviate from the comfortable range of 65 to 75 degrees (5 points each). Data is from FEMA (2025), the AARP Public Policy Institute (2023) and Weather Spark (2024).

- Health care access (30 points): The health care access score includes the average time patients spent in the emergency department before leaving from the visit (10 points), the average Medicare payment per capita for hospital outpatient department services (5 points), the percentage of Medicare beneficiaries enrolled in Medicare Advantage plans (5 points), the percentage of home health agencies rated 4 stars or higher (5 points) and the number of home health and personal care aides per 1,000 seniors (5 points). Data is from the Centers for Medicare & Medicaid Services (2025 and 2022) and the U.S. Bureau of Labor Statistics (2024).

- Traffic safety (5 points): The traffic safety score includes the number of fatal crashes involving seniors (age 65 and over) per 100,000 seniors and the number of senior traffic fatalities per 100,000 seniors (2.5 points each). Data is from the National Highway Traffic Safety Administration (2023).

For each metric, the state that performed the best received the maximum possible score, with all other states scored relative to that benchmark. We added the category scores to calculate each state’s overall score, which is out of 100.

Reference Policy

We love it when people share our findings! If you do, please link back to our original article to credit our research.

Article Sources

Retirement Living writers primarily rely on government data, industry experts and original research from other reputable publications to inform their work. Specific sources for this article include:

- U.S. Census Bureau, “Explore Census Data.” Accessed Oct. 22, 2025.

- NeighborhoodScout, “NeighborhoodScout.” Accessed Oct. 22, 2025.

- Administration for Community Living, “Data Explorer.” Accessed Oct. 22, 2025.

- AARP, “Safety and Quality.” Accessed Oct. 22, 2025.

- Federal Emergency Management Agency, “Map National Risk Index.” Accessed Oct. 22, 2025.

- Weather Spark, “The Weather Year Round Anywhere on Earth.” Accessed Oct. 22, 2025.

- Centers for Medicare & Medicaid Services, “Timely and Effective Care – State.” Accessed Oct. 22, 2025.

- Centers for Medicare & Medicaid Services, “Medicare Geographic Variation – by National, State & County.” Accessed Oct. 22, 2025.

- Centers for Medicare & Medicaid Services, “Monthly Enrollment by State 2025 03.” Accessed Oct. 22, 2025.

- Centers for Medicare & Medicaid Services, “Home Health Care – State by State Data.” Accessed Oct. 22, 2025.

- U.S. Bureau of Labor Statistics, “OEWS Research Estimates by State and Industry.” Accessed Oct. 22, 2025.

- National Highway Traffic Safety Administration, “Fatality Analysis Reporting System (FARS).” Accessed Oct. 22, 2025.

- Federal Emergency Management Agency, “Enhanced State Mitigation Planning: Basics for New Enhanced States.” Accessed Oct. 22, 2025.

- U.S. Census Bureau, “2020 Census: 1 in 6 People in the United States Were 65 and Over.” Accessed Oct. 22, 2025.

10 bucket list trips in the U.S. retirees should take this fall

10 bucket list trips in the U.S. retirees should take this fall

Fall is the golden season for great American getaways

Updated:

Photo by Brice Cooper on Unsplash

Key Insights

- Fall is the perfect time for retirees to explore — cooler weather, fewer crowds, and lower travel costs.

- America’s diverse landscapes shine in autumn, from golden forests to vibrant festivals.

- These ten destinations offer relaxation, beauty, and lifelong memories for travelers ready to savor the season.

Summer is over, kids are back in school, and retirees gain a golden opportunity to hit the road. Autumn’s crisp air and fiery colors turn the United States into a natural masterpiece. Here are ten unforgettable fall trips — no passport required — that belong on every retiree’s bucket list. Depending on where you live, some may be within easy reach.

1. Blue Ridge Parkway, North Carolina & Virginia

Known as “America’s Favorite Drive,” this winding route offers miles of mountain vistas, waterfalls, and vibrant foliage. Stop at quaint Appalachian towns, enjoy easy hiking trails, and visit craft markets in Asheville or Boone.

2. Sedona, Arizona

When summer’s desert heat fades, Sedona’s red rock formations glow under mild fall sunlight. Retirees can enjoy jeep tours, art galleries, and meditation retreats surrounded by stunning natural beauty.

3. Bar Harbor, Maine

Nestled beside Acadia National Park, Bar Harbor is a coastal gem with crisp sea breezes and fiery fall foliage. Enjoy scenic drives along Park Loop Road, lobster dinners, and sunrise views from Cadillac Mountain.

4. Santa Fe, New Mexico

Fall brings cool days and clear skies to Santa Fe’s art-filled streets. The city’s blend of Native American and Spanish heritage, along with vibrant markets and nearby mountain hikes, makes it a rich cultural retreat.

5. Charleston, South Carolina

Autumn’s gentle weather makes it ideal to stroll Charleston’s cobblestone streets, historic gardens, and waterfront promenades. With fewer tourists and thriving food festivals, it’s Southern charm at its most relaxed.

6. Great Smoky Mountains, Tennessee

America’s most-visited national park becomes a painter’s palette in fall. Drive through Clingmans Dome or Cades Cove, spot elk and black bears, and enjoy live bluegrass in nearby Gatlinburg or Pigeon Forge.

7. Napa Valley, California

Harvest season transforms Napa into a swirl of gold and green. Retirees can sip wines amid vineyards, ride hot-air balloons over colorful hills, and indulge in world-class farm-to-table dining.

8. Door County, Wisconsin

This Lake Michigan peninsula is known as the “Cape Cod of the Midwest.” In fall, its orchards brim with apples and cherries, and its coastal villages host harvest festivals and scenic lighthouse tours.

9. New England’s Coastal Route – from Boston to Portland

A road trip along the New England coast offers autumn color with ocean views. Visit Salem’s spooky Halloween festivities, Portsmouth’s seafood shacks, and Maine’s iconic lighthouses under crisp, clear skies.

10. Aspen, Colorado

Before the snow arrives, Aspen’s golden aspen trees create one of the most iconic fall landscapes in America. Retirees can explore mountain trails, attend music festivals, or simply relax by the fire in a cozy lodge.

Fall travel offers retirees lower prices and greater flexibility, but planning ahead still matters. Booking midweek flights, checking for senior travel discounts, and visiting national parks after Labor Day can stretch both comfort and budget.